Home/Blog/How To Do a Reverse Merger Into a Public Shell Company in 9 Not So Easy Steps. Or SPAC in 10!

Leadership Insights

8 min read

How To Do a Reverse Merger Into a Public Shell Company in 9 Not So Easy Steps. Or SPAC in 10!

A reverse merger into a public shell company or completing a SPAC merger can provide a path for companies going public without an IPO. While these strategies can happen faster than a traditional IPO, they are complex transactions involving regulatory compliance, financial restructuring, governance changes, and investor scrutiny. That means they need seasoned C-suite leadership to execute properly.

During the market surge of 2021, SPAC mergers became one of the most talked-about alternatives to the traditional IPO. In a zero-interest-rate environment, special purpose acquisition companies (SPACs) brought many private companies to public markets with fewer barriers than the standard IPO process.

When market conditions tightened and stocks declined, SPAC activity slowed significantly. However, the SPAC market has begun to rebound.

According to data reported by PitchBook, a Morningstar company, there were 144 SPAC IPOs last year, the highest level since 2021. The count has already approached 60 this year.

Hundreds of blank-check companies are actively searching for acquisition targets.

Recent deals demonstrate that, when aligned with investor expectations and growth potential, SPAC transactions remain a viable route to public markets.

But there is one caveat: The most successful companies pursuing this route share one trait: experienced executive leadership guiding the process.

Let’s start with some definitions.

What is a Reverse Merger?

A reverse merger into a public shell company allows a private company to become public by merging with an already-listed company that no longer has active operations. The new company takes over the ticker symbol and installs new leadership, operations, and strategy, all without going through a traditional IPO.

What is a Public Shell?

A public shell company is a publicly traded company that no longer has a meaningful operating business but still maintains its stock listing. Many shells come from companies that ran into trouble (common in industries like biotech) yet still hold value because they are public. Through a reverse merger, a private company can use that shell to enter the public markets while existing shareholders get a chance to recover value.

What is a SPAC?

A SPAC (Special Purpose Acquisition Company) is a company created solely to raise money in an IPO and merge with a private company. Unlike a traditional reverse merger, SPAC deals are typically larger, more structured transactions that involve raising significant capital and incur far higher upfront costs.

What Are the Benefits of a Reverse Merger?

There are several:

Going public gives the acquiring private firm access to the vast liquidity of the public markets.

It’s an option for smaller companies. Typically, an IPO would require a valuation of $200 million or more. A reverse merger can be done by companies with as little as a $40 million valuation.

The reverse merger process is less susceptible to market risk and economic cycles than a conventional IPO.

Owners can more easily sell their shares, although the merger likely will have a lock-up clause limiting the company’s stock sales for a period following the transaction.

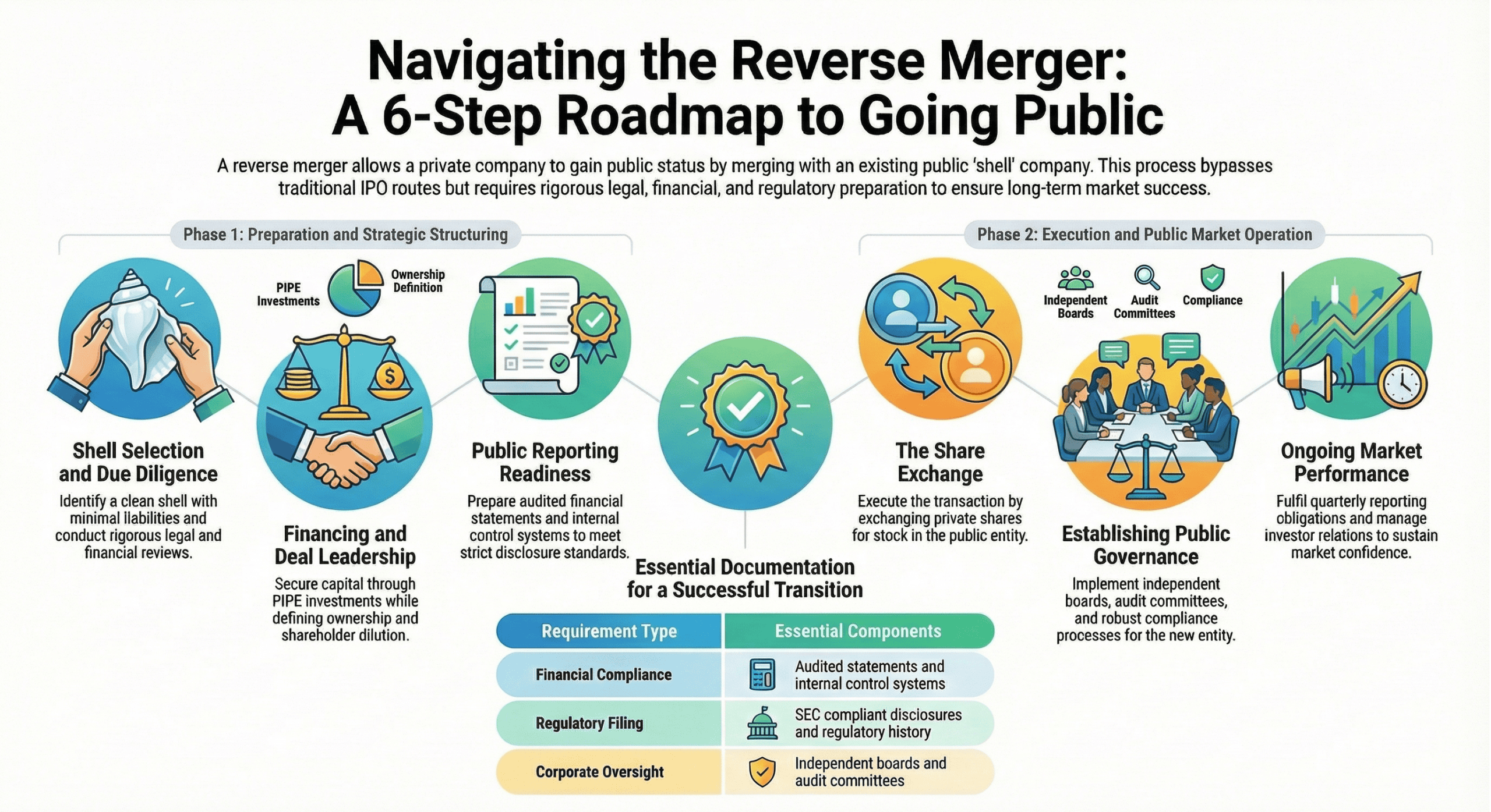

6 Steps to Completing a Reverse Merger Into a Public Shell Company

Step 1: Identify the Right Public Shell Company

Choosing a clean public shell company is critical. The shell must have proper filings, minimal liabilities, and strong regulatory compliance history.

Step 2: Perform Comprehensive Due Diligence

A successful reverse merger transaction requires legal, financial, operational, and compliance reviews. Led by experienced executives, this stage is designed to uncover risks that could derail the deal later. To increase their chances of success, companies often bring in experienced CFOs or interim executives who understand public market due diligence.

Step 3: Structure the Reverse Merger

Deal structure determines ownership, governance, and shareholder dilution. This is where experienced deal leadership becomes essential.

Step 4: Secure Financing or PIPE Investment

Private investment in public equity (PIPE) financing is common and generally tied to investor confidence in the management team. Bringing on a vetted, respected CEO or CFO to lead the process can make a huge difference.

Step 5: Prepare Public Company Financial Reporting

Companies must meet public reporting standards, including:

Audited financial statements

Internal control systems

SEC-compliant disclosures

This is one of the most underestimated phases of the reverse merger process. Experienced CFOs who have been there and done that can lead the finance team through this complex process.

Step 6: Execute the Share Exchange and Close the Transaction

At closing, the private company’s shareholders exchange their shares for stock in the public entity, completing the reverse merger into the public shell.

3 More Steps After the Deal Closes

Once the financial deal is done, it’s time to run the new company. That offers its own leadership challenges, best led by an experienced CEO, to work through these steps:

Step 7: Establish Public Company Governance

Public companies require independent boards, audit committees, and strong compliance processes. Leadership transitions often occur at this stage.

Step 8: Launch Investor Relations and Market Strategy

Once public, the company must communicate effectively with investors, analysts, and regulators.

Step 9: Operate Successfully as a Public Company

Completing a reverse merger is only the beginning. Companies need a C-suite leadership team that knows how to perform in the public market environment, meet quarterly reporting obligations, and manage shareholder expectations.

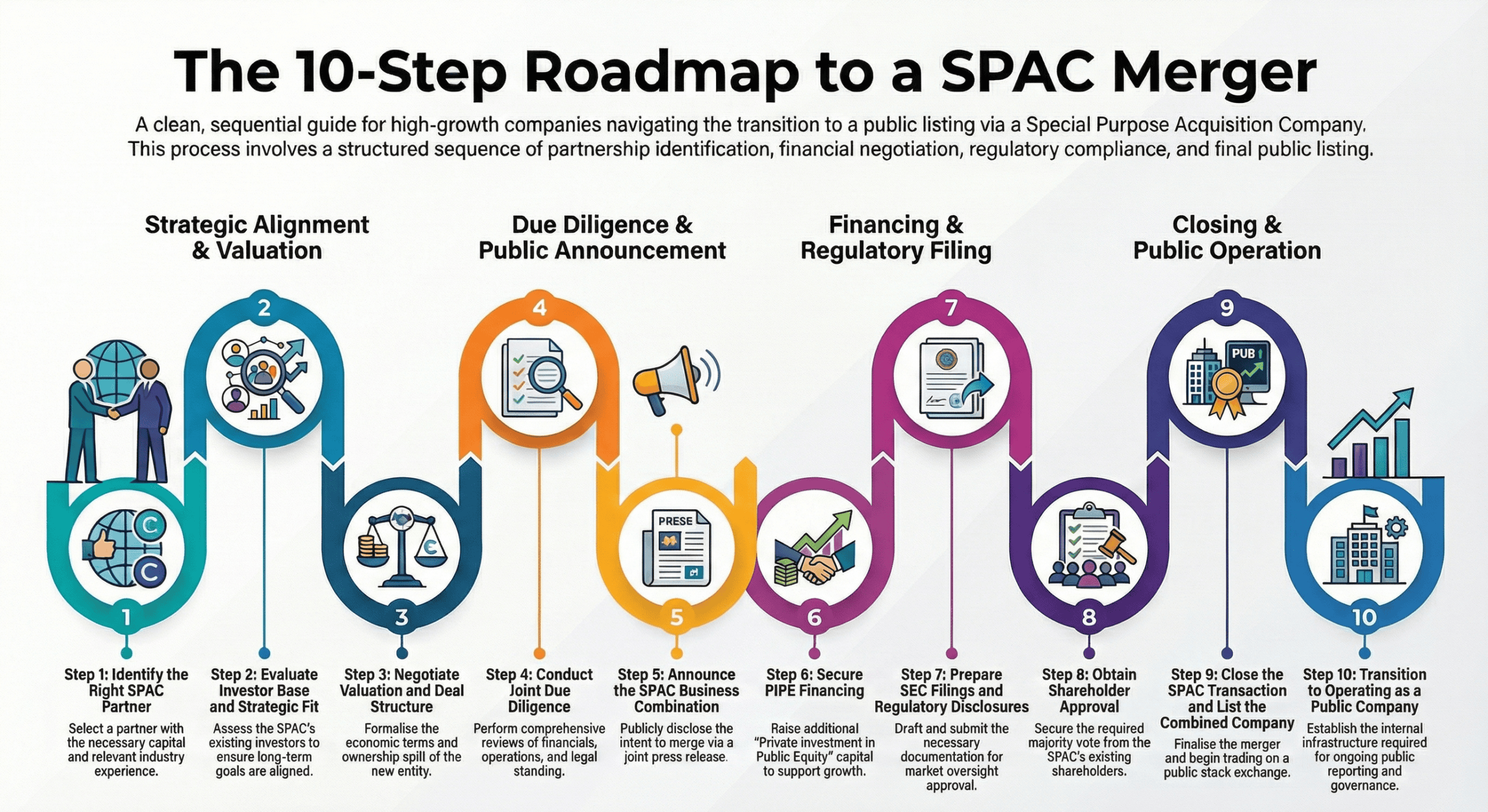

How to Complete a SPAC Merger in 10 Steps

The SPAC merger process is another way to take a company public; it’s particularly popular among deep tech companies, especially quantum computing companies in the AI space, according to Pitchbook.

“SPACs are the standard for quantum companies,” Alex Doll, Ten Eleven Ventures GP and IQM board member, told Pitchbook. “There’s very high confidence in the future growth prospects, so it’s an opportunistic time to choose this route. It’s where the market is and where the growth investors that understand and are already trained on quantum are.”

Plus, Pitchbook notes, deep-tech companies aren’t well-suited for traditional IPOs that rely on historical performance to price initial public offerings.

While SPACs might be enticing, they are much more complex than reverse mergers and can take longer.

The 10 steps to a SPAC:

Identify the right SPAC partner

Evaluate investor base and strategic fit

Negotiate valuation and deal structure

Conduct joint due diligence

Announce the SPAC business combination

Secure PIPE financing

Prepare SEC filings and regulatory disclosures

Obtain shareholder approval

Close the SPAC transaction and list the combined company

Transition to operating as a public company

With hundreds of SPACs still seeking acquisitions, many private companies are exploring the SPAC merger route as an alternative to IPOs, particularly in high-growth sectors like deep tech.

Why Reverse Mergers and SPAC Transactions Benefit From Experienced C-Suite Leadership

Despite the perception that companies can go public faster through a reverse merger or SPAC, the operational complexity often rivals or exceeds that of a traditional IPO.

Key challenges include:

SEC reporting requirements

Corporate governance transformation

Investor communications

Financial system upgrades

Board restructuring

Strategic repositioning as a public company

This is why so many organizations turn to InterimExecs RED Team leaders. They are thoroughly vetted CEOs, CFOs, COOs, and CIOs who have guided companies through reverse mergers, SPAC mergers, and IPO readiness before.

Having leadership that understands public markets can significantly reduce execution risk and improve investor confidence.

If you’re interested in exploring a reverse merger or SPAC for your company, reach out to us for a confidential conversation about how our vetted RED Team interim and fractional executives can spearhead the process for you. Our battle-tested CEO, CFO, and COO leaders can be onsite in as little as 48 hours, assessing the need, creating the plan, and leading the change.

What is a reverse merger into a public shell company?

A reverse merger into a public shell company occurs when a private company merges with an existing public entity, allowing the private company to become publicly traded without completing a traditional IPO.

Is going public through a reverse merger faster than an IPO?

It can be faster, but it is not necessarily easier. The reverse merger process still involves extensive regulatory filings, audits, and governance changes.

What is the SPAC merger process?

A SPAC merger process involves a publicly listed Special Purpose Acquisition Company acquiring a private operating company, effectively taking that company public.

Why are SPACs becoming relevant again?

Recent data highlighted by PitchBook shows a rebound in SPAC IPOs and increased interest in sectors like deep technology and quantum computing, where companies benefit from flexible capital structures.

Why do companies bring in interim executives for reverse mergers or SPAC deals?

Because these are high-stakes transactions, organizations turn to experienced C-suite leaders, like the vetted leaders of the InterimExecs RED Team, who have successfully completed reverse mergers, SPAC transactions, or IPOs before.

ULTIMATE GUIDE TO INTERIM MANAGEMENT

Discover the ins and outs of interim and fractional leadership

First-year Change Agent members have access to the Interim Institute’s 4 hour audio program on the Fundamentals of Interim Management, and a one-hour strategy session to help jumpstart their interim career.

Interim Nonprofit Executive

Join our InterimExecs eNewsletter

This website uses cookies to give visitors the best user experience. To learn more, visit our Privacy Policy.

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. These cookies ensure basic functionalities and security features of the website, anonymously.

Cookie

Duration

Description

cookielawinfo-checkbox-analytics

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Analytics".

cookielawinfo-checkbox-functional

11 months

The cookie is set by GDPR cookie consent to record the user consent for the cookies in the category "Functional".

cookielawinfo-checkbox-necessary

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookies is used to store the user consent for the cookies in the category "Necessary".

cookielawinfo-checkbox-others

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Other.

cookielawinfo-checkbox-performance

11 months

This cookie is set by GDPR Cookie Consent plugin. The cookie is used to store the user consent for the cookies in the category "Performance".

viewed_cookie_policy

11 months

The cookie is set by the GDPR Cookie Consent plugin and is used to store whether or not user has consented to the use of cookies. It does not store any personal data.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.